NIFTSY Tokenomics. Evolution in general tones

Introduction

Tokenomiсs is a neologism formed from the words “economy” and “token” (tokenization), i.e. it is essentially an economy where the main element is the digital asset of decentralised projects.

Tokenomics is a complex phenomenon born at the intersection of technology, social mechanics and economics. Although the process of tokenisation of everything started more than 10 years ago, its zero stage has only just been completed: only now are projects that carry such offline entities (real estate, cars, various activities), protocols that unify such processes and other services appear.

Perhaps, this is why many startups, when creating their own tokenomics, use templates, not realising that standardisation is only possible in general elements, but not where the token plays its main roles — functions. Some go through this stage in the formative stage, others leave it “for later” and thus ruin their ideas in genesis.

Using the example of NIFTSY, we will briefly examine these issues.

The CEO of NIFTSY answers our questions. Shedogubov

Menaskop: So, the first question: where did the tokenomics of NIFTSY start? Let it be a small prehistory of the project’s birth.

А. Shedogubov: The idea of the project was born before the main NFT haip (in autumn 2020): the preconditions for the development of this segment were already visible then. Initially, the project was far from the current concept and underwent a lot of changes.

For example, the initial idea was formed around the market aggregation function of NFT, a kind of aggregator-marketplace. But after a long study and testing of hypotheses, including during Customer Development, it was decided to go down to a lower level and create a protocol applicable to a maximum number of projects.

Even later on, two important developments were added to the project: an oracle for evaluating NFT, and an index providing aggregate data for the market.

Menaskop: Great and understandable. Now a question: “the original version of tokenomics — what was it?”

А. Shedogubov: First of all, a draft version of the roadmap was drawn up and the amount of resources required was calculated, based on 2–3 years for implementation.

After that, we allocated a pool for the implementation of native projects: in the current market understanding, the focus was shifted from these projects to the implementation and implementation of the protocol functions themselves, which allowed us to reduce the requested funding.

In general, we aim to realise a simple concept: “to achieve maximum effect with minimum resources”. At the same time to do this openly and honestly, both for the contributors (token holders) and for the end users of the protocol and its specific implementations.

Initially it was planned to conduct three full rounds of fundraising during the first year and a half, but due to extremely fickle market and based on recommendations of the project’s editors — fundraising was decided to be conducted in the shortest possible time.

Today the project has already received $850 000 in cryptocurrency from funds of different formats. At the same time, we have already implemented the MVP and had an excellent performance with it at the Binance hackathon, where we entered the top 10 projects; and the alpha version will already be completed in the summer. The project is also developing in the information field: we presented it at the largest conference in China (see also) and at a number of online events.

Manaskop: Let’s try a little more detail. What were the intermediate stages and what exactly did the funds advise?

А. Shedogubov: I think the funds’ recommendations are best laid out in chronological order:

The first stage is the sifting out on our part of those who clearly wanted to enter for the sake of quick and high-margin asset sales, although for us, like for all ecosystem participants, the token plays a purely utilitarian role — without it, the protocol will never work directly, as they call it, “without crutches”. So I would call this stage “the guys want to buy Lambo”, i.e. the first quip was that the overall fees were too high, which means that the project needs help. But it was all said with one goal in mind: to quickly and brazenly repackage the marketing, for which to charge very dearly in tokens. Such funds were quickly repurposed as marketing agencies and our screening did not go through. Tokenomics, on the other hand, was generally discussed poorly and in broad strokes.

The second stage was a result of the first one. Already more savvy and, one might say, real, foundations settled on the general thesis: “saw the product, don’t get distracted, we will do the rest”. But even here there was a problem: we were offered to actually reduce the first round and give ALL the marketing to a foundation (at best to related foundations), which could lead to a great dependence of the project on this very foundation and its decisions accordingly. Moreover, the fund offered in an imperative form to “drop out” the funds that had already entered, i.e. to remove them as an “unnecessary burden”, which violated our earlier agreements.

That is why the highest level of dependency and the proposal to break the word, especially on paper, could not be accepted. And tokenomics has once again undergone minimal changes.

Finally we arrived at the third, most protracted but important stage, which I would call “constructive”. What exactly has been proposed?

- Firstly, to reduce the initial rounds;

- Secondly, to split them into seed and private, each with its own allocation (price at the original offer).

- Third, to start actively recruiting KOLs into private for better marketing of the product and specifically for project tokens;

- Fourth, allocate a larger percentage of funds to promoting the product as a whole.

Here we have already tried different models and finally arrived at the one that will be brought out at IDO. But I will still mention a number of other important aspects:

- It was extremely important for us that the funds made the decision to initially freeze the tokens, because we had studied the ICO experience well, including through earlier research within the project of our main adviser, Menaskop. Simply put, we wanted to get away from the scheme: “IDO — pump & dump — perpetual sideways”. And at this stage, all tokens are unfrozen from all categories of counterparties in different stages: this allows to reduce volatility in the market and always have a mechanism at hand to positively influence it.

- The point about creating a liquidity fund was also archival: since the project is primarily focused on integrating DeFi & NFT segments (and then DAO & DEX solutions in general), it would be disastrous to leave the reserve fund small. In addition, the main regulatory mechanism is not incineration, as is common in the market today, but rather the fine-tuning of initial issuance and subsequent token working capital, where it is the fund that serves as an instrument to temporarily freeze any “incinerated” tokens: for example, coming into the secondary market from IDO participants when there is a supply-demand imbalance. Therefore, the fund is there today and its share and importance is high.

- Finally, we are focused specifically on p2p markets and open source solutions, which means that crowdfunding is important to us. And here was probably the most difficult and longest discussion: although the funds are not investing in us (according to SAFT’s), they want to get a complete product and utility token within a foreseeable period of 1–3 years. And we wanted to combine the interests of crowd-participants and those who were included in the seed & private round: especially since at the zero stage we, relatives and friends invested a lot of our efforts and money, and most importantly — time, so that people believed in the project and went after it in the most difficult times. Therefore we left the allocation not only for IDO, but again — for the liquidity pool, for the bounty programme (which looks very worthy and I think we will definitely make a separate publication about it), for the editors and partners, and for all those who help the project. Simply put: we gave people a tool to use the token even before it was technically born.

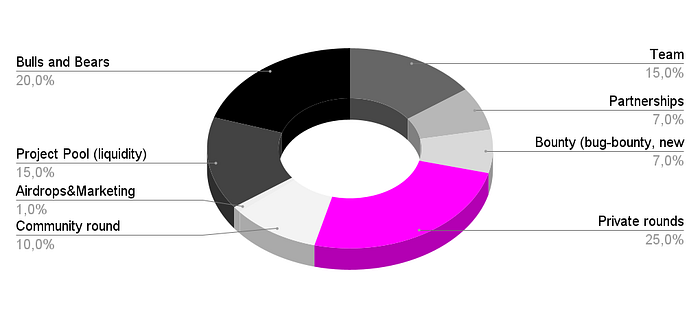

To compare the results, here is a graph on the initial tokenomics:

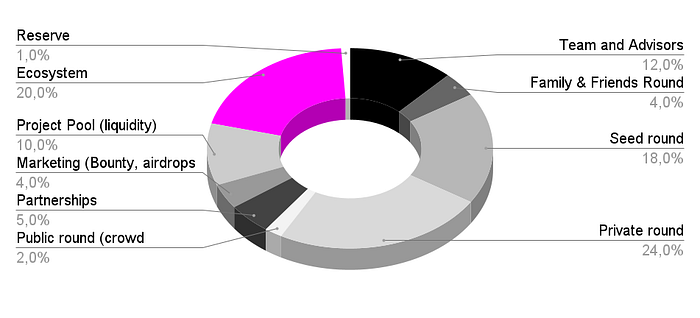

And here’s the pattern for today:

Menaskop: So the story is amazing, but still: what is the final version of tokenomics? Let’s at least outline it.

А. Shedogubov: First of all, actually, we reduced the overall fundraising, because complex tasks cannot be solved in less than 3–5 years, and now it is important to focus on the protocol part and combine it with oracle and index.

We split the initial round into seed and private: they differ primarily in price and the number of tokens as a percentage of the total issue. Why is that? Again, this follows logically from the function of the NIFTSY token: we initially only take funds for product development. At the first stage it is development of MVP (we actually made it at our own expense), and then the refinement to a full alpha. Then, whether we want to or not, we have to enter a very competitive market, and here marketing plays an important role. Hence the different price values: no speculation — a clear calculation of the needs of the moment.

Finally, we are now actively working with KOLs, who actually become our contributors, because they purchase the allocation in the private round and this makes them involved in the process in the most positive sense and at the same time the first testers of the whole system.

Menaskop: I see, that sounds great. Now let’s finish the dialogue on an important note: what did you want to achieve the most in the evolution of initial tokenomics?

А. Shedogubov: First of all, not only I but also the team wanted to achieve optimal tokenomics for the project, funds, and crowdfunding participants, but to do this, it was necessary to make it attractive for initial participants: after all, they have a ready product, but it is still raw and the most difficult for them.

This resulted in a 40–60 split in the direction of the initial participants, which seems to me to be an unavoidable compromise when the priority is to implement the product in the shortest possible time and at the right time for the market. In addition, our forecast was fully justified and the decline in the NFT market began 1–2 months before the deep correction in May. Why? Because the old format of such tokens has become obsolete at lightning speed and the market needs new ideas here and now, which the NIFTSY protocol offers.