NFTs market meta-analysis by NIFTSY

The NFT market is much bigger than digital art, and digital art itself is much bigger than gifs and Musk memes. But that’s not what we’re talking about today, we’re talking about the first, albeit largely approximate, breakdown of the NFT market, which has grown from 2014 (if you believe the crypto lore — the first non-interchangeable token was “born” then) to 2021 by about that many times:

Note that the presented graph can be modified — depending on which estimation parameters and whose data will be included in the meta-analysis of the market. But at the moment we are only interested in the general trend and therefore — have neglected the discrepancies that are described in different sources, especially for the period 2020/2021 and separately — in the early stages of market development: 2014–2016 inclusive (for comparison we can take report #x and report #y).

In this regard — let’s try to answer the simple question “what exactly is under the bonnet of the material?”. The answer is as follows:

- General figures for the market;

- Main development vectors;

- Our forecasts based on p. 1 and p. 2. More precisely — conclusions and short forecasts already on them.

- In general, this article is a systematic one, because from it we will consider each direction separately.

The NFT market is various and interesting, but the first thing that has struck my eye during its searching is hedging function. Here’s exactly what caught my eye: “the exponential growth in this sector has been particularly impressive, especially given that the cryptocurrency bear market has been in full force for much of its early stages of development.” That is, if BTC has become a great hedge for the classic financial market, then NFT (in the broadest possible perspective) could become one for the crypto-asset market itself.

But is it so?

Practice will answer the question, and we will now try to examine the extremely important aspect — numbers and facts, trying to expose the market from this, quantitative, side. To begin with, let’s take sources that are well-known and publicly available:

- Archive №00 — https://coinmarketcap.com/ru/view/collectibles-nfts/

- Archive №01 — https://coinmarketcap.com/nft/collections/

- Archive №02 — https://www.coingecko.com/en/nft

- Archive №03 — https://cryptoslate.com/cryptos/nft/

- Archive №04 — https://coincodex.com/cryptocurrencies/sector/nft/

- Archive №05 — https://nonfungible.com/market/history

- Archive №06 — https://dappradar.com/nft

- Archive №07 — https://cryptoart.io/data

- Archive №08 — https://www.statista.com/topics/7626/crypto-art/

- Archive №09— https://theblockcrypto.com/data/nft-non-fungible-tokens/

Such a detailed description of the archives is necessary because our research is based on a meta-analysis of the market, which is based on the reports mentioned above.

We add the following information to them:

- https://opensea.io/rankings

- statista.com/statistics/1221742/nft-market-capitalisation-worldwide/

- https://dappradar.com/rankings/category/marketplaces

- https://rarible.com/activity

- https://tradingplatforms.com/blog/2021/04/07/nfts-market-cap-experienced-a-cagr-of-187-from-2018-2020-55m-in-revenue-for-2020/

- https://showcase.ethglobal.co

Let us now try to summarise the results:

The first thing to note is the narrow range of evaluation for the new market. Games. Marketplaces. And a dozen more categories (see below). Meanwhile NFT already exists today, not in the distant future (see link #00 and link #01) on, say, Uniswap v. 3.0 and it is (already) NOT a game; and on buying and selling real estate (see example #01, example #02 and others). This approach shows and proves that in many ways this market is still undervalued and yet has excellent prospects for growth in a variety of network indicators:

- the number of active users (so far, it is thousands — tens of thousands of people: given the presence of 7.5 billion on the Planet — the growth prospects are more than impressive, given that the number of active wallets in the crypto industry is estimated at tens to hundreds of millions as of the first quarter of 2021);

- practical implementations — a breakdown of this in the general metrics below and in our next materials;

- other data: from specific Dapps to specialized solutions at the blockchain, protocol and higher layers (which are at least 2–3 more layers).

The second conclusion is by obvious indicators:

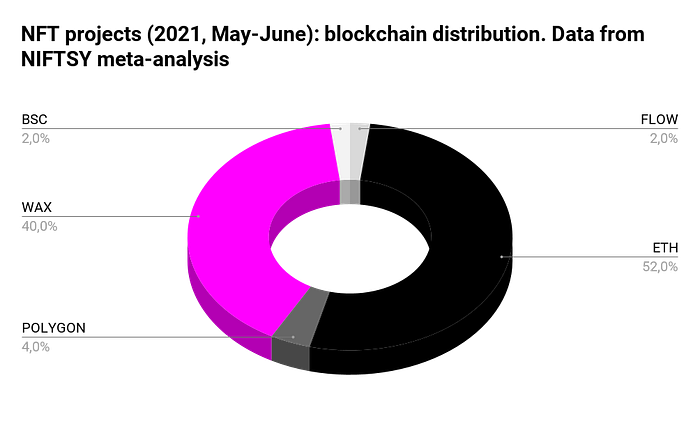

- Ethereum has implemented the most projects, but Wax leads in the number of active traders: one of the next studies will just be parsing the statistics on blockchain solutions for NFT and their prospects. In the tangled conglomerate of consensus, forks and top-tier solutions, there is not as much uniqueness as initially seen.

- First among the categories is the gaming industry (NFT characters, VR properties, etc.). And in general the online aspect of NFT usage seems more obvious so far, although the inevitable process of tokenisation suggests just the opposite: the highly significant role of NFT in the world of unique, offline, objects.

- That said, 2021 and 2020 differ from each other in that the Ethereum ecosystem has begun to lose out to competitors in a number of ways: this is primarily due to “gas wars”, but also due to the fact that the number of developers of different solutions has begun to increase dramatically due to the general heave of DRS (Polkadot, Cosmos, Cardano, WAX, etc.) — decentralised and/or distributed systems.

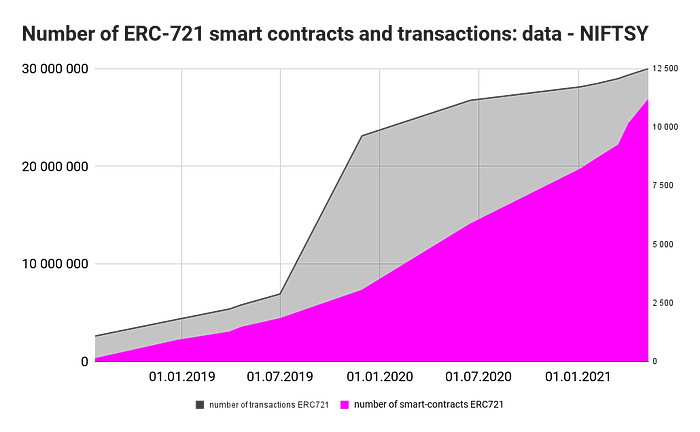

Such sampling can be done not only on DappRadar: on average, aggregators monitor 10–200+ projects, which in itself indicates the possible potential of the market: only a year ago the number of Dapps inside Ethereum ecosystem was just over 2000 — today the growth is over 15%, but, as noted, there is a dramatic increase of decentralized applications on other blockchain solutions and the total number is over 5500, which gives a 150% increase to the previous maximum figure (3470).

In this respect, the following graph is very interesting and highly significant:

At the same time, the weight of individual categories has increased at the expense of the NFT. Let’s start by listing the main ones:

- Games;

- DeFi;

- Gambling;

- Exchange services;

- Collecting;

- Marketplaces;

- Social services;

- High risk projects;

- Others.

Actually, games and collectibles are already largely dependent on NFT, but in the next stage of development we see growth potential in DeFi, marketplaces and decentralised social networks. At the same time, further expansion through the integration of new blockchain solutions corresponds to this trend in the best possible way — this vector is currently being realised: Tezos, Polkadot (primarily through Enjin), Cosmos, Avalanche, Tron, etc. The leadership, on the other hand, may belong according to different indicators: Ethereum (including ETH2 integrations), Flow, WAX, BSC, Enjin and/or other, including completely new projects. At least, the evolution of DeFi products, where YFI, SushiSwap and similar ones beat leaders of Bancor, Kyber and similar solutions of the first wave, gives confidence in this thesis. Moreover — they themselves eventually switched to NFT-integrations (AAVE, YFI, UNI, etc.).

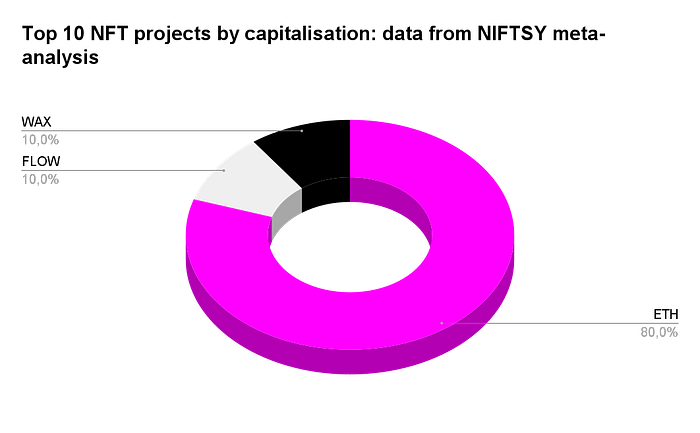

At the moment, however, the following patterns are noticeable. The Ethereum ecosystem ranks first in terms of project capitalisation and by a wide margin:

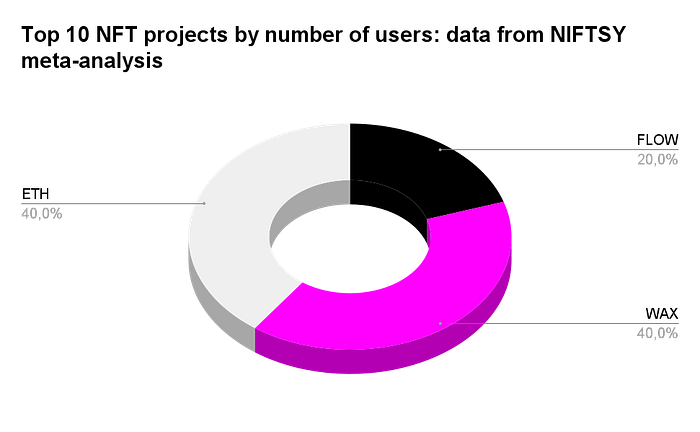

The spread by number of users, however, looks different:

But this is only the first layer of assessment. The second lies on a layer below. First — to quote an excerpt from Uniswap (version 3.0): “As a byproduct of per-LP custom price curves, liquidity positions are no longer fungible and are not represented as ERC20 tokens in the core protocol (just think of liquidity attacks and the concept of “vampire mining” to see why). Instead, LP positions will be represented by non-fungible tokens (NFTs). However, common shared positions can be made fungible (ERC20) via peripheral contracts or through other partner protocols. Additionally, trading fees are no longer automatically reinvested back into the pool on LPs’ behalf. Over time we expect increasingly sophisticated strategies to be tokenized, making it possible for LPs to participate while maintaining a passive user experience. This could include multi-positions, auto-rebalancing to concentrate around the market price, fee reinvestment, lending, and more”.

Simplifying, we can say this: while the market is filled with hype (example #00, example #01, example #02, etc.) around buying and selling NFT in conjunction with all sorts of memes, digital pictures, etc. “art objects”, projects focus on much more interesting, complex and important mechanics. Here are some more examples.

Forward-looking projects

Let’s try to describe those startups that are now trying to buck the vector of the NFT market and turn it into much more than games, collections and digital art tokenisation:

- niftsy.io — the first cross-chain protocol based on tokenisation of payment channels and functional pledging of assets through this, very technical and economical non-trivial, mechanics.

- niftex.org is an NFT sharding platform.

- nftfi.com — not only a supermarket for NFT, but also a mechanism for pledging them through simple and open mechanics.

- immutable.com — top-level (L2) protocol for direct exchange of both ERC-20 and ERC-721 tokens.

- upshot.io — protocol for expert (and possibly objective) real-time evaluation of NFT.

- nftx.org — a platform for creating NFT-backed index funds.

charged.fi — mechanism for creating new format ETFs via NFT wrappers (one NFT can contain different tokens). - nft20.io — a liquidity protocol via NFT: buying and selling via swaps.

- dodonft.io — NFT liquidity protocol, including tokens via swaps.

- safemoon.net — deFi-protocol, which is based on a minimalist functionale and NFT collateral.

- nft.org — a community-driven protocol designed to run applications that support the creation, marketing and exchange of so-called “unplayable” tokens.

We don’t claim to be exhaustive here (at the very least, you can explore NFT implementations in different aspects such as: cs.money, xsolla.com, superrare.co, makersplace.com, viv3.com, foundation.app, mintable.app, mintbase.io, cargo.build, knownorigin. Io, zora.co, whale.me, zed.run, artchain.co, artblocks.io, async.art, ephimera.com, bitski.com, lympo.io, nft.teller.finance), especially since we plan to cover this aspect in detail in a future article, but from this description the near future trends are already obvious:

- Sharding is not only a mechanism for solving problems within blockchain implementations (such as increasing TPS, scaling load sharing, etc.), but also a perfectly overlapping way of sharing risk, profits and other co-ownership parameters in the NFT market.

- Liquidity wrapped in NFT is much more reliable and interesting in terms of possible integrations than liquidity created by interchangeable tokens alone.

- The collateral function is one of the basic features of the NFT-market and its development will largely determine the general evolution of the market and its individual segments. For sure.

The competition between the protocols will eventually lead to the first stage of their unification, because that is where the mass adoption effect lies.

However, there are much more trends. Let’s try to show in broad strokes the less obvious ones.

NFT and not the obvious trends. Prelude

Again — let’s start with a quote: “A fusion of digital and physical with a virtual layer of interlocking hexagons which cover the globe, each has specific coordinates and name, OVR created a space where reality and the virtual can coexist. OVR technology traces your surrounding environment so AR content seamlessly blends into your reality, in a perfect combination between reality and digital. When it comes to viewing historical content in the location it occurred, OVRs digital layer is at the cutting edge of generating unique experiences”.

That is, NFTs for colonising virtual worlds are like ships for the Age of Discovery: they, NFTs, can combine both obvious things from online (say, avatars) and tokenised things from offline (say, fully digitised factories). And that direction, given the nascent deed economy, is almost bottomless.

Or another example: NFT together with an innovative layer of security like tempography gives us the possibility to work not only inside the payment channels, but also to use their possibilities (in particular — liquidity) outside.

Finally, another example of a non-trivial trend (although it is by no means the last one) is NFT as a tool for transferring rights from one DAO to another: after all, no one would deny today that Ethereum, Aragon, and even the Bitcoin blockchain itself as a single Network are developing DAO mechanics further and further. But how painless and easy is it to transfer rights from one decentralised organisation to another? Or how to conduct identification of a MAO created by anonyms who — at the same time — have impeccable transactional reputations (like, say, Satoshi and Anonimus)? Answers to these many related questions — will be forthcoming in our publications. For now, here’s the bottom line on today’s one.

Conclusions

In the medium to long term (1–3 to 5–7 years), we expect the market to grow due to the following trends:

- Overall growth in the number of users of blockchain platforms;

Increased growth in specific blockchain implementations, in which currently the leadership remains with the Ethereum ecosystem, followed by Flow, WAX, BSC and others. There is also potential for growth in DRS such as: Polkadot, Cosmos, Tezos, Tron and Solana. - At this time, by metrics such as: capitalization of projects, the average bill of sale of 1 NFT, the average bill of sale per 1 buyer (seller) — belongs to Ethereum, but the frequency of transactions and the number of sellers / buyers — WAX.

- The development of NFT standards and the increased weighting of non-ERC-721 tokens — also lays the potential for further growth, especially in industries not directly related to collecting and/or digital art.

- To date, NFTs have been involved in a variety of areas. We will highlight a few (in future publications — we will look at all of them in details):

- 1. Protocols that use NFT to implement various functionalities (NIFTSY, UpShot, NFTfi, NFTx, Meme and others).

- 2. Marketplaces (OpenSea, Rarible, EulerBeats, SuperRare, Async Art, Known Origin, Nifty Gateway, Foundation, Portion, MakersPlace, Zora, Mintbase, Mirror (a project that has died), Audius, Auctionity, Pixura, Getpixls, Mooncatrescue, Niftygateway, Blockparty, Known Origin, Myth.Market).

- 3. DeFi (in YFI, NFT is an insurance policy; in UNI, NFT is a liquidity pool position; Aavegotchi uses NFT as secured through AAVE unique characters; Tinlake uses NFT as an opportunity to swap ERC-20 tokens and others, say, AnRKey X).

- 4. Games (aggregators like Alien Worlds, Axie Marketplace, Decentraland Marketplace or Terra Virtua; games proper — CryptoPunks; Cryptokitties; Decentraland and many others).

- 5. The others are all covered in later articles in this series.

- Initial analysis of general market indicators showed that NFT-sellers are not active in crypto-market downturns and this may give rise in the future to an internal hedging tool among crypto-assets: however, for now for a complete argument — existing indicators, especially — in the time slice, are not enough and there are obvious contradictions in this direction.

- At the moment, NFT market is estimated from $1 to $15-$18 billion (depending on project evaluation criteria), but considering such factors as: a) crypto-market growth in 2020–2021 to actually $2 trillion capitalization; b) increase of NFT market share in 2014–2021; c) potential of inherent growth (see above) — this market has all prospects to grow in 10x and more times. And in the medium term. And it is not about valuation in dollars, but about the network effect and intrinsic value to crypto-assets as a whole.

- The main problems, however, are: 01. Verification of NFT collateral: unsecured NFTs can be used for both money laundering and outright fraud; 02. Linking offline and online entities to NFT: it must be unique; 03. Unification of NFT standards: so far, the diversity of platforms and standards is not a problem per se, but rather a growth driver, but without uniform NFT liquidity transfer standards across blockchain platforms and other parameters, it will be extremely difficult to create a market environment that protects the interests of investors as well as developers and direct sellers/buyers.

- The last, but extremely important conclusion for this research is that at the moment, information aggregators (CMC, CoinGecko, DappRadar, etc.) and specialized analytics resources actually focus on classic parameters of project evaluation, while the NFT market, especially in conjunction with DeFi, provides a wider spectrum for objective evaluation of a project, product or any other entities in general: this includes liquidity turnover (collateral), number of reverse sales, commission saved, HODL mechanics, etc.

Therefore, in the following materials, we will elaborate in details:

- Blockchain integrations with NFT;

- NFT marketplaces;

- NFT protocols and their future;

- Other directions (vectors) of evolution.

- And let’s also look at even less obvious trends in this market.

That’s it for today!

P.S. Conducted in conjunction with @Menaskop.